Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Halaman 1 dari 11

Kontak:

Equity & Index Valuation Division

Phone: (6221) 7884 0200 [email protected]

“Pernyataan disclaimer pada halaman akhir merupakan

bagian yang tidak terpisahkan dari dokumen ini” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk Laporan Kedua

Equity Valuation

1 Juni 2015

Target Harga

Terendah Tertinggi 1.065 1.250

Agribisnis

Kinerja Saham

Sumber: Bloomberg, PEFINDO Riset & Konsultasi - Divisi

Valuasi Saham & Indexing

Informasi Saham Rp

Kode saham TBLA

Harga saham 28 Mei 2015 560

Harga Tertinggi 52 minggu terakhir 815

Harga Terendah 52 minggu terakhir 470

Kapitalisasi Pasar Tertinggi 52 minggu

(miliar) 4.354

Kapitalisasi Pasar Terendah 52 minggu (miliar)

2.511

Penilaian Saham Sebelumnya Saat Ini

Terendah 990 1.250

Terendah 845 1.065

Market Value Added & Market Risk

Sumber: Bloomberg, PEFINDO Riset & Konsultasi - Divisi

Valuasi Saham & Indexing

Pemegang Saham (%)

PT Budi Delta Swakarya 27,80

PT Sungai Budi 26,49

Widarto 0,04

Santoso Winata 0,04

Publik (dibawah 5% kepemilikan) 45,63

Tahun yang Manis

PT Tunas Baru Lampung Tbk (TBLA) mengukir sejarahnya sejak tahun 1973, saat pertama kali didirikan. TBLA aktif dalam industri agribisnis, terutama perkebunan kelapa sawit dan produk turunannya, tebu dan produksi gula rafinasi, termasuk perkebunan nanas. TBLA merupakan

bagian dari grup Sungai Budi, salah satu perusahaan pelopor agribisnis.

Saat ini, TBLA memiliki 78.826 hektar (“ha”) area perkebunan berlokasi di Lampung, Sumatera Selatan dan Kalimantan Barat. TBLA mendistribusikan produknya ke luar dan dalam negeri. Salah satu produknya yang terkenal di dalam negeri adalah minyak goreng “Rose Brand”. Untuk mempertahankan pertumbuhannya di masa datang, TBLA telah menambah jumlah area tertanamnya (menjadi 6.000 ha, per September 2014) di Kalimantan Barat, membangun pabrik

pengolahan gula di Terbanggi – Lampung, pabrik pengolahan kelapa sawit di Surabaya dan Lampung, membangun pabrik biodiesel baru di Lampung, dan memperluas area tebu di Lampung.

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 2 dari 11

Penyesuaian Target Harga

Kami membuat beberapa penyesuaian untuk proyeksi kami sebelumnya, dan menyesuaikan target harga kami menjadi Rp1.065 – Rp1.250 per saham, berdasarkan pertimbangan sebagai berikut:

Permintaan CPO global dan domestik masih ada. Meskipun harga jual rata-rata CPO global menurun, kami melihat bahwa permintaan global untuk CPO Indonesia masih ada. Persediaan yang menipis di Tiongkok selama 1Q2015, akan menyebabkan permintaan yang signifikan dari CPO Indonesia di kuartal berikutnya. Sementara India terus menunjukkan tren peningkatan permintaan CPO Indonesia. Di dalam negeri, peraturan baru untuk meningkatkan kandungan minyak nabati pada biodiesel, secara signifikan mempengaruhi

produksi. Dari 0,4 juta kilo liter ("KL") biodiesel di tahun 2011, meningkat menjadi 2,9 juta KL per September 2014, yang diterjemahkan menjadi sekitar 10 miliar KL produksi CPO, naik dari sekitar 6,5 miliar KL pada tahun 2011.

Merasakan efek dari pabrik gula baru. Setelah pabrik penyulingan gula baru selesai dibangun pada akhir tahun 2013, pendapatan TBLA dari bisnis pengolahan gula melonjak secara signifikan. Volume penjualan gula rafinasi

pada tahun 2014 adalah 115.134 ton, jauh lebih tinggi dari tahun 2013 (hanya 7.445 ton). Ke depan, kami melihat bahwa bisnis dari pengolahan gula akan memberikan kontribusi yang lebih tinggi untuk pendapatan TBLA, karena mereka baru tahun pertama memproduksi dari pabrik gula baru.

Kinerja yang luar biasa. Kami melihat bahwa kinerja TBLA sangat mengagumkan di 2014. Pendapatan melonjak 71% yoy atau mencapai Rp3,7 triliun, didukung pertumbuhan yang kuat dari bisnis pengolahan gula.

Penurunan rugi bersih transaksi mata uang asing menciptakan peningkatan laba sebelum pajak sebesar 373% yoy, atau sebesar Rp562 miliar. Di masa depan, kami melihat bahwa TBLA akan terus membukukan peningkatan pendapatan, terutama dari bisnis pengolahan gula, seiring dioperasikannya pabrik penyulingan gula baru secara bertahap hingga mencapai pemanfaatan yang optimal.

Perubahan asumsi risk-free rate, equity premium, dan beta menjadi 8,19%,

2,22%, dan 0,60x. Prospek Usaha Kami melihat bahwa permintaan global untuk CPO Indonesia masih ada, karena CPO merupakan komoditas yang tetap dibutuhkan oleh masyarakat. Peningkatan populasi dan masyarakat kelas menengah juga menciptakan permintaan yang

stabil akan CPO Indonesia. Di dalam negeri, berlakunya peraturan peningkatan kandungan minyak nabati dalam bahan bakar biodiesel, membuat permintaan CPO stabil. Sementara di bisnis gula, kesenjangan yang lebar antara permintaan dan penawaran gula rafinasi, seperti ditunjukkan dengan seberapa cepat kuota impor gula mentah terpenuhi pada tahun 2014, membuat prospek bisnis ini masih cerah. Mengingat ini, kami melihat bahwa prospek TBLA, sebagai perusahaan yang aktif dalam bisnis ini tetap optimis. Sebagai hasilnya, kami

memperkirakan bahwa pendapatan TBLA akan tumbuh minimal 11,5% CAGR selama periode tahun 2014-2019. Tabel 1: Ringkasan Kinerja

2012 2013 2014 2015P 2016P

Pendapatan [Rp miliar] 3.806 3.705 6.338 6.691 7.439

Laba Sebelum Pajak [Rp miliar] 311 119 562 780 930

Laba Bersih [Rp miliar] 242 84 433 580 691

EPS [Rp] 45 16 81 109 129

Pertumbuhan EPS [%] (42) (65) 414 34 19

P/E [x] 10,8 29,8 9,3 5,2* 4,3*

PBV [x] 1,5 1,4 1,6 1,0* 0,8*

Sumber: PT Tunas Baru Lampung Tbk, Estimasi PEFINDO Divisi Valuasi Saham & Indexing

Catatan: *) Berdasarkan harga saham tanggal 29 Mei 2015 – Rp560/saham

PARAMETER INVESTASI

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 3 dari 11

Overview Ekonomi Indonesia Tahun 2015: Diekspektasikan Tumbuh Lebih

Kencang Pada tahun 2015, kami mengekspektasikan tingkat pertumbuhan ekonomi untuk berada di kisaran 5,3% -5,7%, ditopang oleh konsumsi swasta meningkat, inflasi yang terkendali dan tingkat suku bunga yang stabil. Sejauh ini, tekanan inflasi yang relatif rendah selama 1Q2015 telah membuat daya beli masyarakat stabil, digambarkan oleh Indeks Keyakinan Konsumen yang relatif stabil selama Februari 2015. Belanja Pemerintah yang cukup besar, dengan ekspansi APBN-nya juga

akan berperan sebagai katalis yang dapat mendorong ekonomi lebih cepat tahun ini. Investasi sektor swasta diekspektasikan baru dapat mendorong ekonomi di akhir tahun setelah terlihat prospek ekonomi dan politik yang lebih jelas dan pemerintah akan mampu mengeluarkan dan memberlakukan peraturan yang lebih kondusif, serta menyelesaikan hambatan di sektor logistik dan infrastruktur untuk memacu investasi sektor swasta. Realisasi investasi di 1Q2014 adalah Rp106,6 triliun, sementara realisasi investasi diharapkan 1Q2015 adalah Rp115 triliun.

Namun, kami harus mencatat bahwa keadaan defisit transaksi berjalan dan volatilitas Rupiah merupakan faktor risiko utama untuk pencapaian pertumbuhan ekonomi yang lebih cepat tahun ini

Gambar 1: Realisasi Investasi

1Q2014 – 1Q2015

Sumber : Badan Koordinasi Penanaman Modal, PEFINDO Riset & Konsultasi – Divisi Valuasi

Saham & Indexing

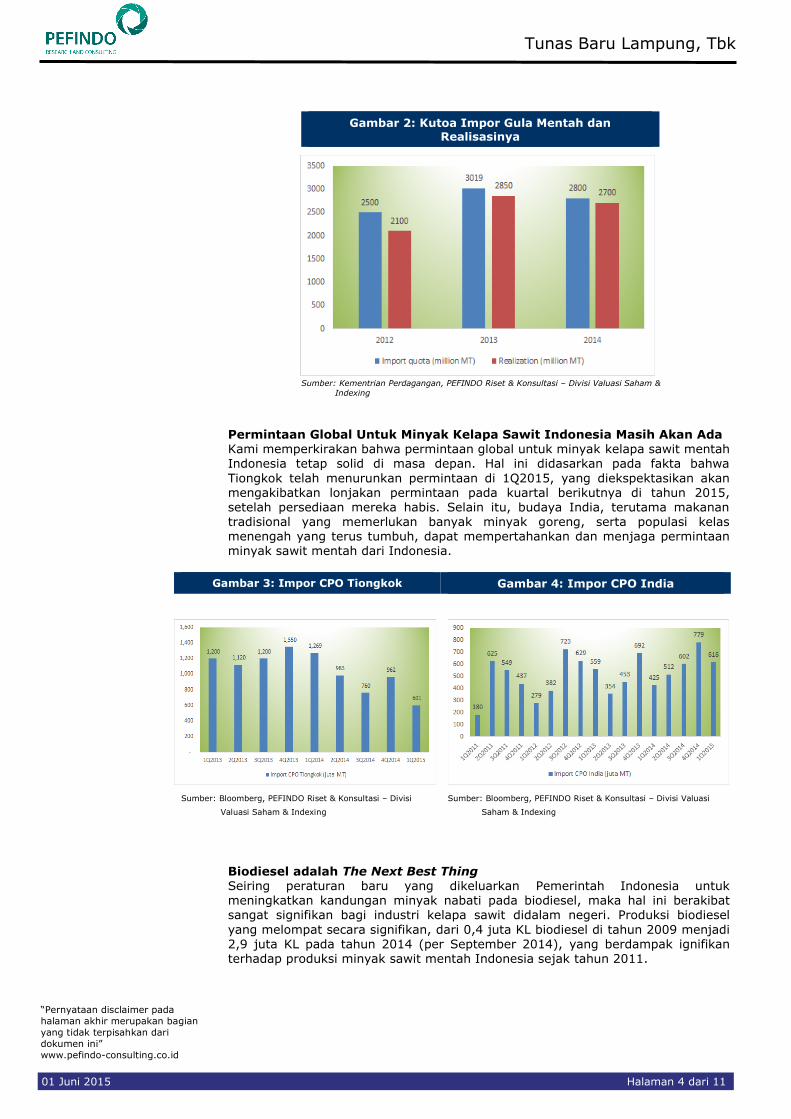

Permintaan Gula Rafinasi Tetap Tinggi Untuk melindungi petani tebu dalam negeri, Pemerintah Indonesia telah

membatasi impor gula mentah, dengan memberlakukan maksimal kuota. Namun, kami memperkirakan bahwa kuota tersebut tidak akan berpengaruh, karena permintaan, terutama untuk gula industri, hanya dapat dipenuhi dengan mengimpor gula mentah untuk kemudian diperhalus di dalam negeri. Pada tahun 2014, kuota maksimum untuk gula mentah yang diimpor adalah 2,8 juta MT, tapi

sampai November 2014 sudah mencapai 2,7 juta MT, menggambarkan

permintaan yang besar dari pasar domestik. Oleh karenanya, volume gula mentah yang masuk ke pasar domestik cukup besar.

MAKROEKONOMI DAN INDUSTRI

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 4 dari 11

Gambar 2: Kutoa Impor Gula Mentah dan Realisasinya

Sumber: Kementrian Perdagangan, PEFINDO Riset & Konsultasi – Divisi Valuasi Saham &

Indexing

Permintaan Global Untuk Minyak Kelapa Sawit Indonesia Masih Akan Ada Kami memperkirakan bahwa permintaan global untuk minyak kelapa sawit mentah Indonesia tetap solid di masa depan. Hal ini didasarkan pada fakta bahwa

Tiongkok telah menurunkan permintaan di 1Q2015, yang diekspektasikan akan mengakibatkan lonjakan permintaan pada kuartal berikutnya di tahun 2015, setelah persediaan mereka habis. Selain itu, budaya India, terutama makanan tradisional yang memerlukan banyak minyak goreng, serta populasi kelas menengah yang terus tumbuh, dapat mempertahankan dan menjaga permintaan minyak sawit mentah dari Indonesia.

Gambar 3: Impor CPO Tiongkok Gambar 4: Impor CPO India

Sumber: Bloomberg, PEFINDO Riset & Konsultasi – Divisi

Valuasi Saham & Indexing

Sumber: Bloomberg, PEFINDO Riset & Konsultasi – Divisi Valuasi

Saham & Indexing

Biodiesel adalah The Next Best Thing Seiring peraturan baru yang dikeluarkan Pemerintah Indonesia untuk meningkatkan kandungan minyak nabati pada biodiesel, maka hal ini berakibat sangat signifikan bagi industri kelapa sawit didalam negeri. Produksi biodiesel

yang melompat secara signifikan, dari 0,4 juta KL biodiesel di tahun 2009 menjadi 2,9 juta KL pada tahun 2014 (per September 2014), yang berdampak ignifikan terhadap produksi minyak sawit mentah Indonesia sejak tahun 2011.

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 5 dari 11

Gambar 5: Produksi CPO Indonesia

Sumber: Bloomberg, PEFINDO Riset & Konsultasi - Divisi Valuasi Saham & Indexing

Kontribusi yang Kuat dari Bisnis Gula Selama periode tahun 2014, kami melihat bahwa bisnis gula TBLA telah berubah

menjadi "bisnis yang manis", dengan kontribusi 14,5% (termasuk pendapatan dari tebu). Kontribusi semacam itu jauh lebih tinggi dari tahun 2013 yaitu 3,1%. Pertumbuhan tersebut terutama disebabkan bisnis pengolahan gula, yang baru dimulai pada akhir tahun 2013 (mengimpor gula mentah dan kemudian

memprosesnya lebih lanjut menjadi gula halus), setelah pembangunan pabrik penyulingan gula baru telah selesai. Volume penjualan gula rafinasi pada 2014 adalah 115.134 ton, sementara pada tahun 2013 hanya 7.445 ton. Ke depan, kami

percaya bahwa TBLA akan mampu memproduksi gula mentah sendiri, karena perusahaan kini menanam lebih banyak tanaman tebu untuk memenuhi kebutuhan mereka. Pada 1Q2015, kontribusi dari bisnis gula sedikit turun menjadi 9,3%. Tetapi hal itu dapat dimengerti karena tanaman tebu belum panen pada periode tersebut. Kami

percaya, kontribusi pendapatan dari bisnis gula akan lebih tinggi pada tahun 2015, karena TBLA sekarang dalam proses konversi areal perkebunan kelapa sawit yang “tua” ke areal tebu.

Gambar 6: Breakdown Pendapatan TBLA per Produk

Sumber: PT Tunas Baru Lampung Tbk, PEFINDO Riset & Konsultasi - Divisi Valuasi Saham & Indexing

BISNIS

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 6 dari 11

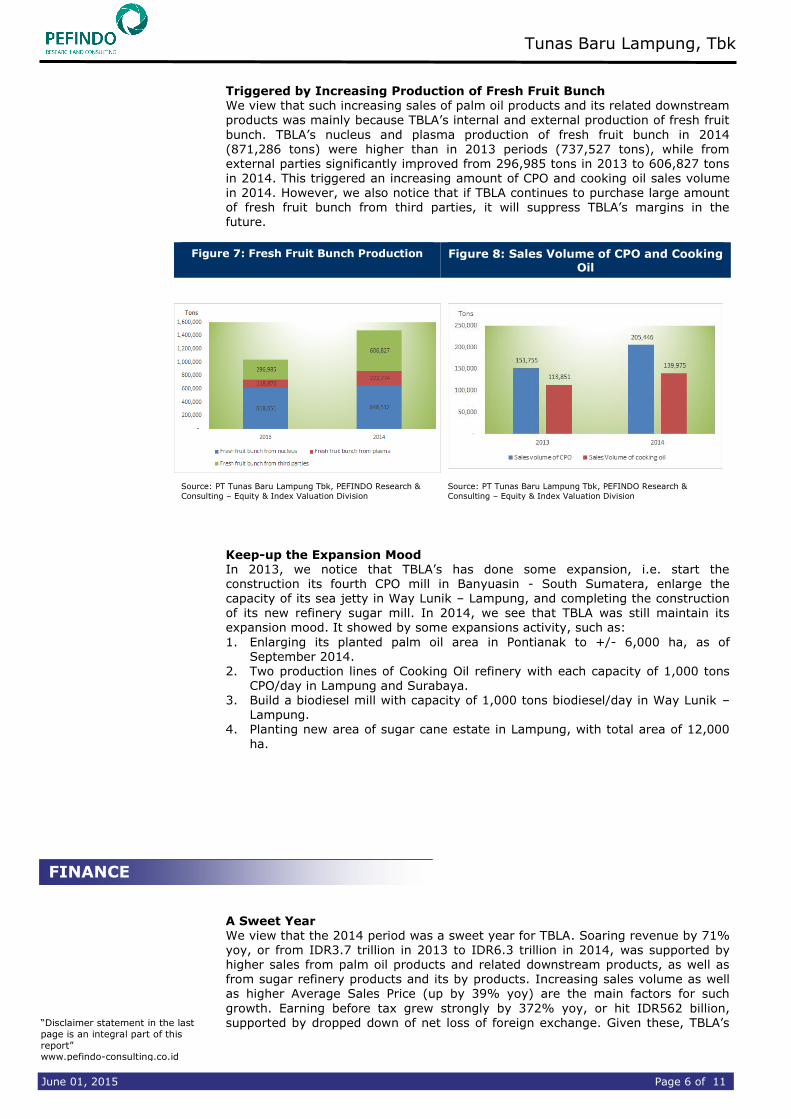

Dipicu oleh Peningkatan Produksi Tandan Buah Segar

Kami melihat bahwa peningkatan penjualan untuk produk minyak kelapa sawit dan produk hilir terkait lainnya, terutama dikarenakan peningkatan produksi internal dan eksternal tandan buah segar TBLA. Produksi tandan buah segar dari petani inti

dan plasma TBLA pada tahun 2014 mencapai 871.286 ton lebih tinggi dibandingkan tahun 2013 (737.527 ton), sedangkan dari pihak eksternal secara signifikan meningkat dari 296.985 ton pada tahun 2013 menjadi 606.827 ton pada tahun 2014. Hal ini memicu peningkatan jumlah volume penjualan CPO dan minyak goreng pada tahun 2014. Namun, kami juga melihat bahwa jika TBLA terus membeli sejumlah besar tandan buah segar dari pihak ketiga, maka hal itu akan menekan margin TBLA di masa depan.

Gambar 7: Produksi Tandan Buah Segar Gambar 8: Volume Penjualan Minyak Kelapa Sawit dan Minyak Goreng

Sumber: PT Tunas Baru Lampung Tbk, PEFINDO Riset &

Konsultasi – Divisi Valuasi Saham & Indexing

Sumber: PT Tunas Baru Lampung Tbk, PEFINDO Riset & Konsultasi

– Divisi Valuasi Saham & Indexing

Menjaga Keinginan Berekspansi Pada tahun 2013, kami melihat bahwa TBLA telah melakukan beberapa ekspansi,

yaitu memulai pembangunan pabrik CPO keempat di Banyuasin - Sumatera Selatan, memperbesar kapasitas dermaga laut di Way Lunik - Lampung, dan

menyelesaikan pembangunan pabrik gula baru. Pada tahun 2014, kami melihat bahwa TBLA masih mempertahankan keinginannya untuk ekspansi. Hal ini ditunjukkan dengan beberapa aktivitas ekspansi, seperti: 1. Perluasan area tertanam kelapa sawit di Pontianak menjadi +/- 6,000 ha, per

September 2014. 2. Dua lini produksi penyulingan minyak goreng dengan masing-masing kapasitas

1.000 ton minyak kelapa sawit/hari di Lampung dan Surabaya. 3. Membangun pabrik biodiesel dengan kapasitas produksi 1.000 ton

biodiesel/hari di Way Lunik – Lampung. 4. Penambahan area tertanam untuk tebu di Lampung, dengan total area 12.000

ha.

Tahun yang Manis

Kami melihat bahwa tahun 2014 merupakan tahun yang manis bagi TBLA. Pendapatan melonjak 71% yoy, atau dari Rp3,7 triliun pada tahun 2013 menjadi

Rp6,3 triliun di tahun 2014, didukung oleh naiknya penjualan minyak kelapa sawit dan produk hilir terkait lainnya, serta dari produk gula rafinasi dan produk sampingannya. Meningkatnya volume penjualan dan rata-rata harga jual (naik

KEUANGAN

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 7 dari 11

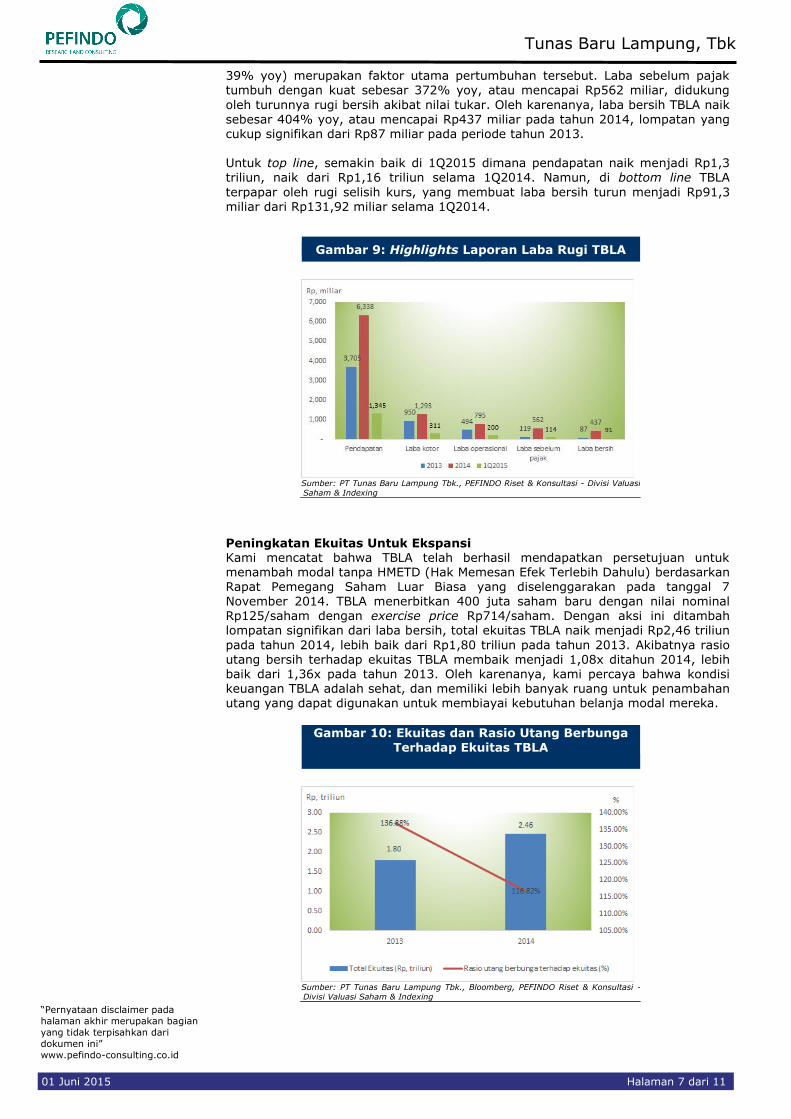

39% yoy) merupakan faktor utama pertumbuhan tersebut. Laba sebelum pajak tumbuh dengan kuat sebesar 372% yoy, atau mencapai Rp562 miliar, didukung

oleh turunnya rugi bersih akibat nilai tukar. Oleh karenanya, laba bersih TBLA naik

sebesar 404% yoy, atau mencapai Rp437 miliar pada tahun 2014, lompatan yang cukup signifikan dari Rp87 miliar pada periode tahun 2013. Untuk top line, semakin baik di 1Q2015 dimana pendapatan naik menjadi Rp1,3 triliun, naik dari Rp1,16 triliun selama 1Q2014. Namun, di bottom line TBLA

terpapar oleh rugi selisih kurs, yang membuat laba bersih turun menjadi Rp91,3 miliar dari Rp131,92 miliar selama 1Q2014.

Gambar 9: Highlights Laporan Laba Rugi TBLA

Sumber: PT Tunas Baru Lampung Tbk., PEFINDO Riset & Konsultasi - Divisi Valuasi Saham & Indexing

Peningkatan Ekuitas Untuk Ekspansi Kami mencatat bahwa TBLA telah berhasil mendapatkan persetujuan untuk menambah modal tanpa HMETD (Hak Memesan Efek Terlebih Dahulu) berdasarkan Rapat Pemegang Saham Luar Biasa yang diselenggarakan pada tanggal 7

November 2014. TBLA menerbitkan 400 juta saham baru dengan nilai nominal Rp125/saham dengan exercise price Rp714/saham. Dengan aksi ini ditambah lompatan signifikan dari laba bersih, total ekuitas TBLA naik menjadi Rp2,46 triliun

pada tahun 2014, lebih baik dari Rp1,80 triliun pada tahun 2013. Akibatnya rasio utang bersih terhadap ekuitas TBLA membaik menjadi 1,08x ditahun 2014, lebih baik dari 1,36x pada tahun 2013. Oleh karenanya, kami percaya bahwa kondisi keuangan TBLA adalah sehat, dan memiliki lebih banyak ruang untuk penambahan utang yang dapat digunakan untuk membiayai kebutuhan belanja modal mereka.

Gambar 10: Ekuitas dan Rasio Utang Berbunga Terhadap Ekuitas TBLA

Sumber: PT Tunas Baru Lampung Tbk., Bloomberg, PEFINDO Riset & Konsultasi - Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 8 dari 11

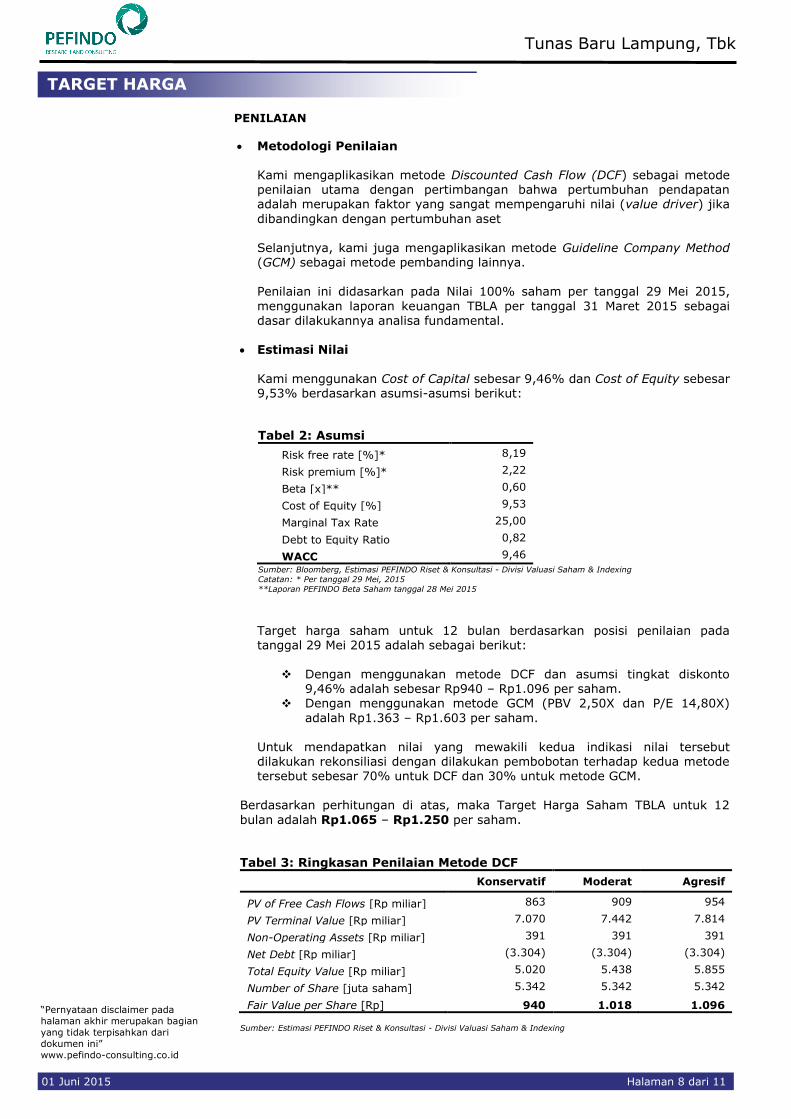

PENILAIAN

Metodologi Penilaian Kami mengaplikasikan metode Discounted Cash Flow (DCF) sebagai metode penilaian utama dengan pertimbangan bahwa pertumbuhan pendapatan adalah merupakan faktor yang sangat mempengaruhi nilai (value driver) jika

dibandingkan dengan pertumbuhan aset Selanjutnya, kami juga mengaplikasikan metode Guideline Company Method (GCM) sebagai metode pembanding lainnya. Penilaian ini didasarkan pada Nilai 100% saham per tanggal 29 Mei 2015,

menggunakan laporan keuangan TBLA per tanggal 31 Maret 2015 sebagai dasar dilakukannya analisa fundamental.

Estimasi Nilai

Kami menggunakan Cost of Capital sebesar 9,46% dan Cost of Equity sebesar 9,53% berdasarkan asumsi-asumsi berikut:

Tabel 2: Asumsi

Risk free rate [%]* 8,19

Risk premium [%]* 2,22

Beta [x]** 0,60

Cost of Equity [%] 9,53

Marginal Tax Rate 25,00

Debt to Equity Ratio 0,82

WACC 9,46

Sumber: Bloomberg, Estimasi PEFINDO Riset & Konsultasi - Divisi Valuasi Saham & Indexing

Catatan: * Per tanggal 29 Mei, 2015

**Laporan PEFINDO Beta Saham tanggal 28 Mei 2015

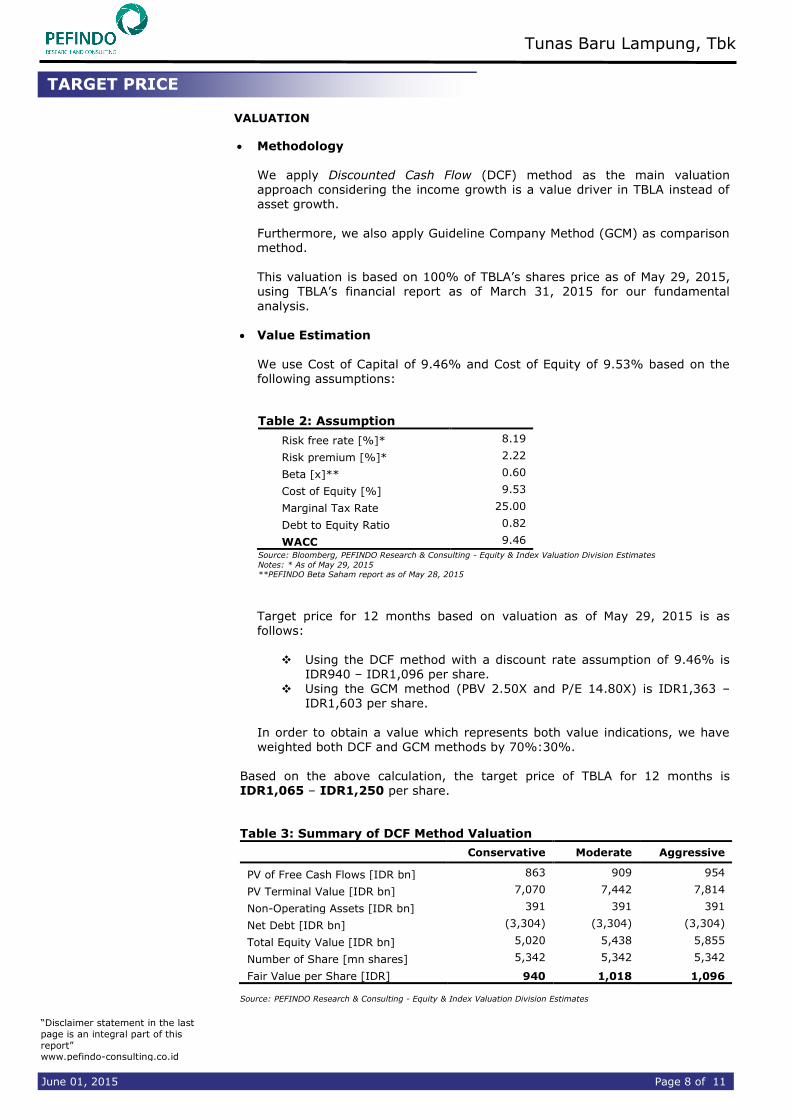

Target harga saham untuk 12 bulan berdasarkan posisi penilaian pada tanggal 29 Mei 2015 adalah sebagai berikut:

Dengan menggunakan metode DCF dan asumsi tingkat diskonto

9,46% adalah sebesar Rp940 – Rp1.096 per saham. Dengan menggunakan metode GCM (PBV 2,50X dan P/E 14,80X)

adalah Rp1.363 – Rp1.603 per saham.

Untuk mendapatkan nilai yang mewakili kedua indikasi nilai tersebut dilakukan rekonsiliasi dengan dilakukan pembobotan terhadap kedua metode tersebut sebesar 70% untuk DCF dan 30% untuk metode GCM.

Berdasarkan perhitungan di atas, maka Target Harga Saham TBLA untuk 12

bulan adalah Rp1.065 – Rp1.250 per saham.

Tabel 3: Ringkasan Penilaian Metode DCF

Konservatif Moderat Agresif

PV of Free Cash Flows [Rp miliar] 863 909 954

PV Terminal Value [Rp miliar] 7.070 7.442 7.814

Non-Operating Assets [Rp miliar] 391 391 391

Net Debt [Rp miliar] (3.304) (3.304) (3.304)

Total Equity Value [Rp miliar] 5.020 5.438 5.855

Number of Share [juta saham] 5.342 5.342 5.342

Fair Value per Share [Rp] 940 1.018 1.096

Sumber: Estimasi PEFINDO Riset & Konsultasi - Divisi Valuasi Saham & Indexing

TARGET HARGA

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 9 dari 11

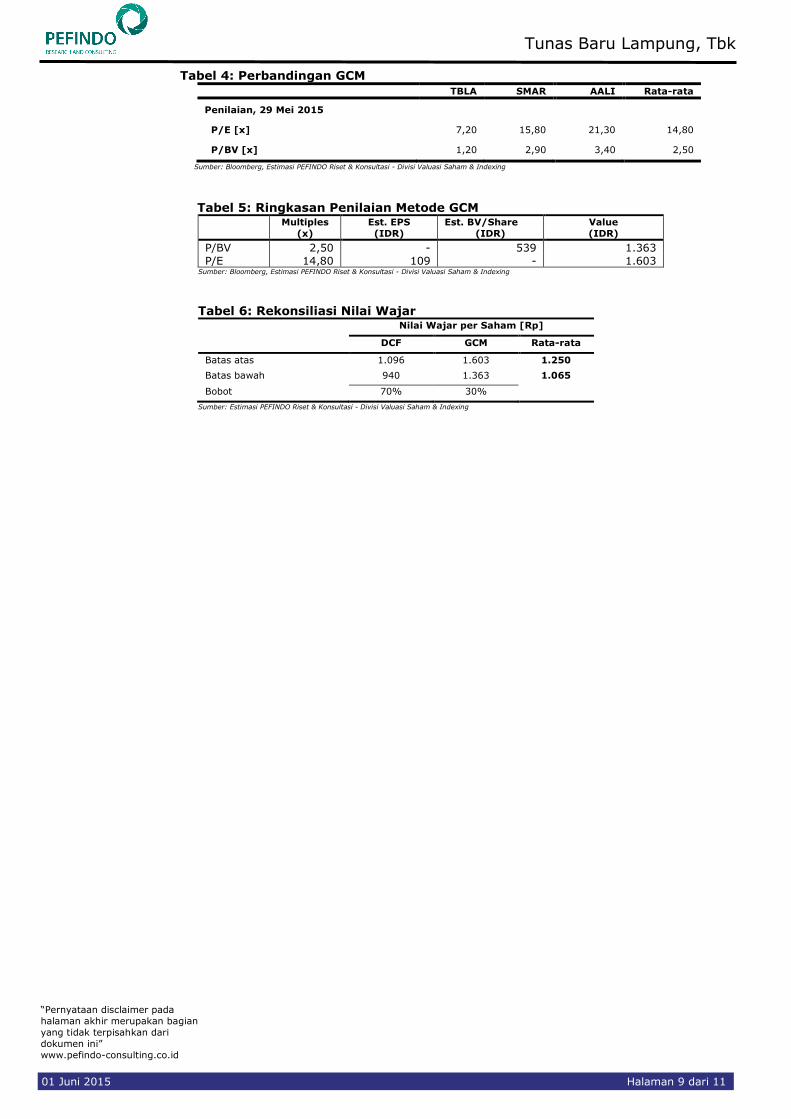

Tabel 4: Perbandingan GCM

TBLA SMAR AALI Rata-rata

Penilaian, 29 Mei 2015

P/E [x] 7,20 15,80 21,30 14,80

P/BV [x] 1,20 2,90 3,40 2,50

Sumber: Bloomberg, Estimasi PEFINDO Riset & Konsultasi - Divisi Valuasi Saham & Indexing

Tabel 5: Ringkasan Penilaian Metode GCM

Multiples

(x)

Est. EPS

(IDR)

Est. BV/Share

(IDR)

Value

(IDR)

P/BV 2,50 - 539 1.363

P/E 14,80 109 - 1.603 Sumber: Bloomberg, Estimasi PEFINDO Riset & Konsultasi - Divisi Valuasi Saham & Indexing

Tabel 6: Rekonsiliasi Nilai Wajar Nilai Wajar per Saham [Rp]

DCF GCM Rata-rata

Batas atas 1.096 1.603 1.250

Batas bawah 940 1.363 1.065

Bobot 70% 30%

Sumber: Estimasi PEFINDO Riset & Konsultasi - Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 10 dari 11

Tabel 7: Laporan Laba Rugi Konsolidasian

(Rp miliar) 2012 2013 2014 2015P 2016P

Penjualan 3.806 3.705 6.338 6.691 7.439

Harga Pokok

Penjualan (2.778) (2.756) (5.045) (5.114) (5.612)

Laba Kotor 1.028 950 1.293 1.577 1.827

Beban Operasi (717) (831) (730) (796) (898)

Laba Sebelum

Pajak 311 119 562 780 930

Pajak (67) (33) (126) (195) (232)

Laba Bersih 242 84 433 580 691

Sumber: PT Tunas Baru Lampung Tbk., PEFINDO Riset & Konsultasi - Divisi Valuasi

Saham & Indexing Tabel 8: Laporan Posisi Keuangan Konsolidasian

(Rp miliar) 2012 2013 2014 2015P 2016P

Aset

Aset Lancar

Kas dan Setara Kas 559 658 529 941 250

Piutang Usaha 385 416 711 632 703

Persediaan 649 795 956 1,033 1,337

Aset Lancar

Lainnya 724 673 664 919 1,018

Total Aset Lancar 2,318 2,543 2,860 3,524 3,308

Tanaman 1,042 1,195 1,402 1,609 2,050

Aset Tetap 1,750 2,321 2,844 2,321 2,844

Aset Lainnya 87 153 222 158 185

Total Aset 5,198 6,212 7,328 7,613 8,386

Liabilitas

Hutang Usaha 250 183 292 540 592

Pinjaman Jk.

Pendek 1,111 2,010 2,183 2,227 2,384

Kewajiban Jk. Pendek Lainnya

99 77 115 134 156

Pinjaman Jk.

Panjang 1,804 1,961 2,049 1,581 1,597

Pinjaman Jk.

Panjang Lainnya 174 184 224 253 286

Total Liabilitas 3,438 4,414 4,864 4,735 5,016

Total Ekuitas 1,759 1,798 2,464 2,878 3,370

Source: PT Tunas Baru Lampung Tbk., Estimasi PEFINDO Divisi Valuasi Saham & Indexing

Gambar 11: P/E dan P/BV Historis

Sumber: PT Tunas Baru Lampung Tbk., PEFINDO Riset & Konsultasi - Divisi

Valuasi Saham & Indexing

Gambar 12: ROA, ROE dan TAT Historis

Sumber: PT Tunas Baru Lampung Tbk., PEFINDO Riset & Konsultasi - Divisi

Valuasi Saham & Indexing

Tabel 9: Rasio Penting

Rasio 2012 2013 2014 2015P 2016P

Pertumbuhan (%)

Pendapatan 2,0 (2,6) 71,0 5,6 11,2

Laba sebelum

pajak (42,4) (61,7) 372,3 38,8 19,1

Laba bersih (42,3) (65,1) 413,6 33,8 19,1

Profitabilitas (%)

Marjin laba kotor 27,0 25,6 20,4 23,6 24,6

Marjin laba

sebelum pajak 8,2 3,2 8,9 11,7 12,5

Marjin laba bersih 6,3 2,3 6,8 8,7 9,3

ROA 4,6 1,4 5,9 7,6 8,2

ROE 13,7 4,7 17,6 20,2 20,5

Solvabilitas (%)

Debt to Equity 2,0 2,5 2,0 1,6 1,5

Interest Bearing

Debt to Equity 1,2 1,7 1,4 1,0 0,9

Debt to Asset 0,7 0,7 0,7 0,6 0,6

Sumber : PT Tunas Baru Lampung Tbk., Estimasi PEFINDO Riset & Konsultasi -

Divisi Valuasi Saham & Indexing

“Pernyataan disclaimer pada

halaman akhir merupakan bagian

yang tidak terpisahkan dari

dokumen ini”

www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

01 Juni 2015 Halaman 11 dari 11

DISCLAIMER

Laporan ini dibuat berdasarkan sumber-sumber yang kami anggap terpercaya dan dapat diandalkan. Namun kami tidak menjamin kelengkapan, keakuratan atau kecukupannya. Dengan demikian kami tidak bertanggung jawab atas segala keputusan investasi yang diambil berdasarkan laporan ini. Adapun asumsi, opini, dan perkiraan merupakan hasil dari pertimbangan internal kami per tanggal penilaian (cut off date),

dan kami dapat mengubah pertimbangan diatas sewaktu-waktu tanpa pemberitahuan terlebih dahulu. Kami tidak bertanggung jawab atas kekeliruan atau kelalaian yang terjadi akibat penggunaan laporan ini. Kinerja dimasa lalu tidak selalu dapat dijadikan acuan hasil masa depan. Laporan ini bukan merupakan rekomendasi penawaran, pembelian atau menahan suatu saham tertentu. Laporan ini mungkin tidak sesuai untuk beberapa investor. Seluruh opini dalam laporan ini telah disampaikan dengan itikad baik, namun sewaktu-waktu dapat berubah tanpa pemberitahuan terlebih dahulu, dan disajikan dengan benar

per tanggal diterbitkan laporan ini. Harga, nilai, atau pendapatan dari setiap saham Perseroan yang disajikan dalam laporan ini kemungkinan dapat lebih rendah dari harapan pemodal, dan pemodal juga mungkin mendapatkan pengembalian yang lebih rendah dari nilai investasi yang ditanamkan. Investasi didefinisikan sebagai pendapatan yang kemungkinan besar diterima dimasa depan, namun nilai dari pendapatan yang akan diterima tersebut kemungkinan besar juga akan berfluktuasi. Untuk saham Perseroan yang penyajian laporan keuangannya didenominasi dalam mata uang selain Rupiah, perubahan

nilai tukar mata uang tersebut kemungkinan dapat menurunkan nilai, harga, atau pendapatan investasi pemodal. Informasi dalam laporan ini bukan merupakan pertimbangan pajak dalam mengambil suatu keputusan investasi. Target harga saham dalam Laporan ini merupakan nilai fundamental, bukan merupakan Nilai Pasar Wajar, dan bukan merupakan harga acuan transaksi yang diwajibkan oleh peraturan perundang-undangan yang berlaku.

Laporan target harga saham yang diterbitkan oleh PT Pefindo Riset Konsultasi (PRK) atau PEFINDO Research and Consulting bukan merupakan rekomendasi untuk membeli, menjual, atau menahan suatu saham tertentu, dan tidak dapat dianggap sebagai nasehat investasi oleh PRK yang berhubungan dengan cakupan Jasa kepada, atau kaitannya kepada, beberapa pihak, termasuk emiten, penasehat keuangan, pialang saham, investment banks, institusi keuangan dan perantara keuangan, dalam kaitannya menerima imbalan atau keuntungan lainnya dari pihak tersebut.

Laporan ini tidak ditujukan untuk pemodal tertentu dan tidak dapat dijadikan bagian dari tujuan investasi

terhadap suatu saham dan juga bukan merupakan rekomendasi investasi terhadap suatu saham tertentu atau suatu strategi investasi. Sebelum melakukan tindakan dari hasil laporan ini, pemodal disarankan untuk mempertimbangkan terlebih dahulu kesesuaian situasi dan kondisi dan, jika dibutuhkan, mintalah bantuan penasehat keuangan.

PEFINDO memisahkan kegiatan Valuasi Saham dengan kegiatan Pemeringkatan untuk menjaga independensi dan objektivitas dari proses dan produk kegiatan analitis. PEFINDO telah menetapkan kebijakan dan prosedur untuk menjaga kerahasiaan informasi non-publik tertentu yang diterima sehubungan dengan proses analitis. Keseluruhan proses, metodologi dan database yang digunakan dalam penyusunan Laporan Target Harga Referensi Saham ini secara keseluruhan adalah berbeda dengan proses, metodologi dan database yang digunakan PEFINDO dalam melakukan pemeringkatan.

Laporan ini dibuat dan disiapkan PRK dengan tujuan untuk meningkatkan transparansi harga saham yang tercatat di Bursa Efek Indonesia. Laporan ini juga bebas dari pengaruh tekanan atau paksaan dari Bursa maupun Perseroan yang dinilai. PRK akan menerima imbalan dari Perseroan dan Bursa Efek Indonesia untuk 2 (dua) kali pelaporan per tahun. Untuk keterangan lebih lanjut, dapat mengunjungi website kami di http://www.pefindo-consulting.co.id

Laporan ini dibuat dan disiapkan oleh PT PEFINDO Riset Konsultasi - Divisi Valuasi Saham dan Indexing. Di Indonesia Laporan ini dipublikasikan pada website kami dan juga pada website Bursa Efek Indonesia.

Page 1 of 11

Contact:

Equity & Index Valuation Division

Phone: (6221) 7884 0200 [email protected]

“Disclaimer statement in the last page is an integral part

of this report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk Secondary Report

Equity Valuation

June 1, 2015

Target Price

Low High 1,065 1,250

Agribusiness Industry

Stock Performance Chart

Source : Bloomberg, PEFINDO Research & Consulting -

Equity & Index Valuation Division

Stock Information IDR

Ticker code TBLA

Market price as of April 28, 2015 560

Market price – 52 week high 815

Market price – 52 week low 470

Market cap – 52 week high (bn) 4,354

Market cap – 52 week low (bn) 2,511

Stock Valuation Last Current

High 990 1,250

Low 845 1,065

Market Value Added & Market Risk

Source : Bloomberg, PEFINDO Research & Consulting -

Equity & Index Valuation Division

Shareholders (%)

PT Budi Delta Swakarya 27.80

PT Sungai Budi 26.49

Widarto 0.04

Santoso Winata 0.04

Public (each below 5% of ownerships) 45.63

A Sweet Year

PT Tunas Baru Lampung Tbk (TBLA) traces its history back to 1973, when it was first established. TBLA is actively involves in the agribusiness industry, particularly in the plantation of palm oil and producing its derivatives products, sugar cane and sugar refinery

production, as well as pineapple plantation. TBLA is a member of

Sungai Budi group, one of the pioneer in the agricultural based products. Currently, TBLA owns around 78,826 hectares (“ha”) of plantation areas, located in Lampung, South Sumatera and West Kalimantan. TBLA distributes their product inside and outside of Indonesia. One of its well-known domestic products is its palm cooking oil with brand name of “Rose Brand”. With regard to sustaining their growth in the future, TBLA has already increased its planted area of

palm oil (amounted to 6,000 ha, as of September 2014), in West Kalimantan, constructing a sugar mill in Terbanggi – Lampung, palm oil refinery in Surabaya and Lampung, constructing new biodiesel mill in Lampung, and enlarging its sugarcane plantation area in Lampung.

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 2 of 11

Target Price Adjustment We made several adjustments to our previous projections, and adjust our target price to a range of IDR1,065 – IDR1,250 per share, based on the following considerations:

Global and domestic demand of CPO is still there. Despite the dropping average

sales price of global CPO, we view that global demand for Indonesia’s CPO is still there. Depleted inventories in China during 1Q2015, will cause significant demand of Indonesia’s CPO in the next quarters. While India continues to show growing demand of Indonesia’s CPO. In domestic, the new regulation to increase the content of vegetable oil in the biodiesel, significantly affect the

production. From 0.4 million kilo liters (“KL”) of biodiesel in 2011, it rose to 2.9 million Kl as of September 2014, which translates into around a production of total 10,000 million KL of CPO, up from around 6,500 million KL in 2011.

Feel the effect of the new sugar refinery mill. After the new sugar refinery mill has been completed in the late 2013, TBLA’s revenue from sugar refinery business was soaring-up significantly. Sales volume of refined sugar in 2014

was 115,134 tons, much higher than in 2013 (only 7,445 tons). Going forward, we view that the sugar refinery business will provide higher contribution to TBLA’s revenue, since it was only their first year of production from the new sugar refinery mill.

Superb performance. We view that TBLA has accomplished such astonishing performance in 2014. Its revenue soared by 71% yoy or reach IDR3.7 trillion, on the back of strong growth from sugar refinery business. Decreasing net loss

of foreign exchange creates a rose of earning before tax by 373% yoy, or amounted to IDR562 billion. In the future, we see that TBLA will continue to book an increasing revenue, especially from sugar refinery business, as the new sugar refinery mill will gradually operates at optimum utilization.

Change of Risk-free rate, equity premium, and beta assumption to 8.19%, 2.22%, and 0.60x respectively.

Business Prospects We view that global demand for Indonesian CPO is still there, since CPO is constitutes as a commodity that continuously needed by people. Increasing population and middle-class society also create a stable demand for Indonesia’s CPO. In domestic, the enactment regulation of increasing vegetable oil content in biodiesel fuel, keeps the demand for CPO stable. While in sugar business, a deep

gap between demand and supply for refinery sugar, as showed by how quick the import quota was being filled in 2014, makes the prospect of this business remains bright. Given this, we view that TBLA’s prospect, as a company that actively participates in these business remains in the upbeat condition. As a result, we estimate that TBLA’s revenue will grow by at least 11.5% CAGR during 2014 – 2019 periods.

Table 1: Performance Summary

2012 2013 2014 2015P 2016P

Net sales (IDR bn) 3,806 3,705 6,338 6,691 7,439

Pre-tax profit (IDR bn) 311 119 562 780 930

Net profit (IDR bn) 242 84 433 580 691

EPS (IDR) 45 16 81 109 129

EPS Growth (%) (42) (65) 414 34 19

P/E (x) 10.8 29.8 9.3 5.2* 4.3*

PBV (x) 1.5 1.4 1.6 1.0* 0.8*

Source: PT Tunas Baru Lampung Tbk, PEFINDO Research & Consulting - Equity & Index Valuation Division Estimates

Notes: *) Based on Share Price as of May 29, 2015 – IDR560/share

INVESTMENT PARAMETERS

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 3 of 11

Indonesia Economy Overview in 2015: Expected to Grow Faster

In 2015, we expect the economic growth rate to yield in the region of 5.3%-5.7%, sustained by an increasing private consumption, controlled inflation and stable interest rate environment. So far, the relatively low inflationary pressure during 1Q2015 has kept people purchasing power stable, depicted by Confident Consumer Index that is relatively stable during February 2015. Government spending with its expansive 2015 state budget will also play as the catalyst that can propel the faster economic growth this year. Private sector investment can only be expected

to give more weight to the economic growth later in the year until after the businesses can see brighter economic and political outlook more clearly and the government will have been able to issue and implement more conducive regulations and de-bottleneck logistic and infrastructure strains to spur private sector investment. Investment realization in 1Q2014 was IDR106.6 trillion, while expected investment realization in 1Q2015 was IDR115 trillion. However, we should note that the state of current account deficit and Rupiah volatility are major

risk factors to the achievement of faster economic growth this year.

Figure 1: Investment Realization

1Q2014 – 1Q2015

Source: Investment Coordination Board, PEFINDO Research & Consulting - Equity & Index

Valuation Division

Demand for Refined Sugar Remains Large To protect domestic sugarcane farmers, the Indonesian Government is limiting the import of raw sugar, by enacting a maximum quota. However, we foresee that such quota will not be affected, since the demand, especially industry sugar, can

only be fulfilled by importing raw sugar and refined it domestically. In 2014, the maximum quota for imported raw sugar was 2.8 million MT, but until November 2014 it already reached 2.7 million MT, picturing a massive demand from domestic market. Given this, large volume of sugar has entered domestic market illegally.

MACROECONOMY AND INDUSTRY

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 4 of 11

Figure 2: Raw Sugar Import Quota and Realization

Source: Ministry of Trade, PEFINDO Research & Consulting - Equity & Index Valuation

Division

Global Demand for Indonesia’s Crude Palm Oil Will Still There We estimate that the global demand for Indonesia’s crude palm oil remains solid in the future. It is based on the fact that China has lowered its demand in 1Q2015, which indicate a surge demand for the next quarters in 2015, after their inventories was depleted. Beside that, India’s culture, especially its traditional food

that requires lots of palm cooking oil, as well as its growing middle class population, sustain and keep dragging-up the demand for Indonesia’s crude palm oil.

Figure 3: China’s Import of CPO Figure 4: India’s Import of CPO

1,200 1,120

1,200

1,350 1,269

983

760

962

601

-

200

400

600

800

1,000

1,200

1,400

1,600

1Q2013 2Q2013 3Q2013 4Q2013 1Q2014 2Q2014 3Q2014 4Q2014 1Q2015

China's import of CPO (million MT)

180

625

549

437

279

382

723

629559

354

453

692

425

512

602

779

616

0

100

200

300

400

500

600

700

800

900

India's imported CPO (million MT)

Source: Bloomberg, PEFINDO Research & Consulting – Equity

& Index Valuation Division

Source: Bloomberg, PEFINDO Research & Consulting – Equity

& Index Valuation Division

Biodiesel is The Next Best Thing

As the Indonesian Government issued a new regulation to increase the content of

vegetable oil in the biodiesel, the effect for the domestic palm oil industry is just massive. With significant jump of production, or from 0.4 KLof biodiesel in 2009 to 2.9 million KL in 2014 (as of September 2014), it dragged a significant impact to the production of Indonesia crude palm oil since 2011.

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 5 of 11

Figure 5: Indonesia’s CPO Production

Source: Bloomberg, PEFINDO Research & Consulting - Equity & Index Valuation Division

Strong Contribution from Sugar Business During 2014 periods, we view that TBLA’s sugar business has turned into a “sweet business”, with a contribution of 14.5% (including revenue from sugar cane) in

2014. Such contribution was much higher than 2013 period of 3.1%. Such growth was mainly due the sugar refinery business, which just started at the late period of 2013 (importing raw sugar and then process it further into refined sugar), after

the construction of new sugar refinery mill has been completed. Sales volume of refined sugar in 2014 was 115,134 tons, while it was only 7,445 tons in 2013. Going forward, we believe that TBLA will be able to produce its raw sugar itself as

the company now planting more sugar cane plants to fulfill their requirement. In 1Q2015, the contribution from sugar business were slightly dropped to 9.3%. But, it is understandable since the sugar cane plants were not harvesting yet in such period. We believe, the revenue contribution from sugar business will be higher in 2015, since TBLA is now in the process of converting its “old” palm oil plantation area into sugar cane area.

Figure 6: TBLA’s Revenue Breakdown by Products

Source: PT Tunas Baru Lampung Tbk, PEFINDO Research & Consulting - Equity & Index

Valuation Division

BUSINESS

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 6 of 11

Triggered by Increasing Production of Fresh Fruit Bunch We view that such increasing sales of palm oil products and its related downstream

products was mainly because TBLA’s internal and external production of fresh fruit

bunch. TBLA’s nucleus and plasma production of fresh fruit bunch in 2014 (871,286 tons) were higher than in 2013 periods (737,527 tons), while from external parties significantly improved from 296,985 tons in 2013 to 606,827 tons in 2014. This triggered an increasing amount of CPO and cooking oil sales volume in 2014. However, we also notice that if TBLA continues to purchase large amount of fresh fruit bunch from third parties, it will suppress TBLA’s margins in the future.

Figure 7: Fresh Fruit Bunch Production Figure 8: Sales Volume of CPO and Cooking Oil

Source: PT Tunas Baru Lampung Tbk, PEFINDO Research &

Consulting – Equity & Index Valuation Division

Source: PT Tunas Baru Lampung Tbk, PEFINDO Research &

Consulting – Equity & Index Valuation Division

Keep-up the Expansion Mood In 2013, we notice that TBLA’s has done some expansion, i.e. start the construction its fourth CPO mill in Banyuasin - South Sumatera, enlarge the capacity of its sea jetty in Way Lunik – Lampung, and completing the construction

of its new refinery sugar mill. In 2014, we see that TBLA was still maintain its expansion mood. It showed by some expansions activity, such as:

1. Enlarging its planted palm oil area in Pontianak to +/- 6,000 ha, as of September 2014.

2. Two production lines of Cooking Oil refinery with each capacity of 1,000 tons CPO/day in Lampung and Surabaya.

3. Build a biodiesel mill with capacity of 1,000 tons biodiesel/day in Way Lunik – Lampung.

4. Planting new area of sugar cane estate in Lampung, with total area of 12,000

ha.

A Sweet Year We view that the 2014 period was a sweet year for TBLA. Soaring revenue by 71% yoy, or from IDR3.7 trillion in 2013 to IDR6.3 trillion in 2014, was supported by higher sales from palm oil products and related downstream products, as well as from sugar refinery products and its by products. Increasing sales volume as well as higher Average Sales Price (up by 39% yoy) are the main factors for such

growth. Earning before tax grew strongly by 372% yoy, or hit IDR562 billion, supported by dropped down of net loss of foreign exchange. Given these, TBLA’s

FINANCE

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 7 of 11

net income rose by 404% yoy, or reached IDR437 billion in 2014, a giant leap from IDR87 billion in 2013 period.

For top line, it gets better in 1Q2015 as its revenue rose to IDR1.3 trillion, up from IDR1.16 trillion during 1Q2014. However, at the bottom line TBLA was suffered by the loss on foreign exchange, which made its net profit dropped to IDR91.3 billion from IDR131.92 billion during 1Q2014.

Figure 9: TBLA’s Highlights of Income Statement

Source: PT Tunas Baru Lampung Tbk., PEFINDO Research & Consulting - Equity &

Index Valuation Division

Increasing Equity for Expansion We note that TBLA has successfully get an approval to increase its capital without Rights Issue (pre-emptive rights) based on the Extraordinary Stockholders’

Meeting held on November 7, 2014. TBLA issued 400 million new shares with nominal amount of IDR125/share with exercise price of IDR714/share. With such action plus a significant leap of net income, TBLA’s total equity improved to IDR2.46 trillion in 2014, better than IDR1.80 trillion in 2013. As a result TBLA’s net

debt to equity ratio improved to 1.08x in 2014, better than 1.36x in 2013. Given this, we believe that TBLA’s financial condition is healthier, and has more room for debt to finance their capex requirement.

Figure 10: TBLA’s Equities and Net Debt to Equity Ratio,

Source: PT Tunas Baru Lampung Tbk., Bloomberg, PEFINDO Research & Consulting

- Equity & Index Valuation Division

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 8 of 11

VALUATION

Methodology We apply Discounted Cash Flow (DCF) method as the main valuation approach considering the income growth is a value driver in TBLA instead of asset growth.

Furthermore, we also apply Guideline Company Method (GCM) as comparison method. This valuation is based on 100% of TBLA’s shares price as of May 29, 2015, using TBLA’s financial report as of March 31, 2015 for our fundamental

analysis.

Value Estimation

We use Cost of Capital of 9.46% and Cost of Equity of 9.53% based on the following assumptions:

Table 2: Assumption

Risk free rate [%]* 8.19

Risk premium [%]* 2.22

Beta [x]** 0.60

Cost of Equity [%] 9.53

Marginal Tax Rate 25.00

Debt to Equity Ratio 0.82

WACC 9.46

Source: Bloomberg, PEFINDO Research & Consulting - Equity & Index Valuation Division Estimates

Notes: * As of May 29, 2015 **PEFINDO Beta Saham report as of May 28, 2015

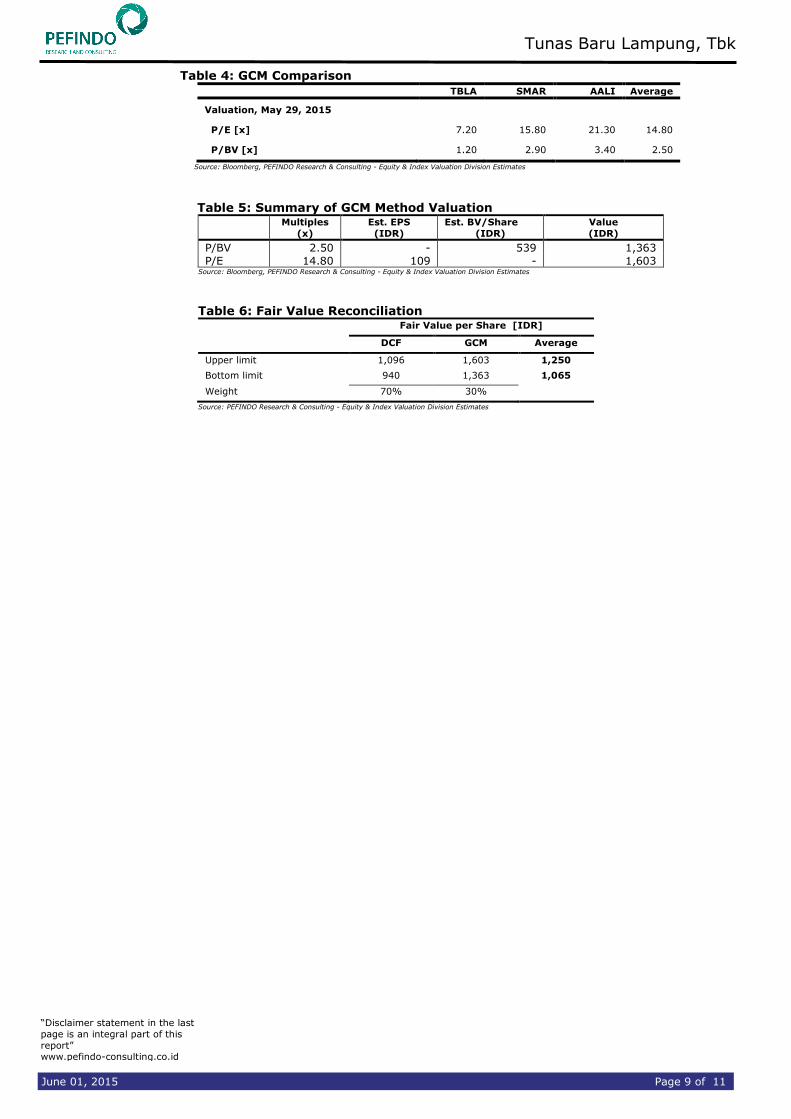

Target price for 12 months based on valuation as of May 29, 2015 is as follows:

Using the DCF method with a discount rate assumption of 9.46% is IDR940 – IDR1,096 per share.

Using the GCM method (PBV 2.50X and P/E 14.80X) is IDR1,363 – IDR1,603 per share.

In order to obtain a value which represents both value indications, we have weighted both DCF and GCM methods by 70%:30%.

Based on the above calculation, the target price of TBLA for 12 months is IDR1,065 – IDR1,250 per share.

Table 3: Summary of DCF Method Valuation

Conservative Moderate Aggressive

PV of Free Cash Flows [IDR bn] 863 909 954

PV Terminal Value [IDR bn] 7,070 7,442 7,814

Non-Operating Assets [IDR bn] 391 391 391

Net Debt [IDR bn] (3,304) (3,304) (3,304)

Total Equity Value [IDR bn] 5,020 5,438 5,855

Number of Share [mn shares] 5,342 5,342 5,342

Fair Value per Share [IDR] 940 1,018 1,096 Source: PEFINDO Research & Consulting - Equity & Index Valuation Division Estimates

TARGET PRICE

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 9 of 11

Table 4: GCM Comparison

TBLA SMAR AALI Average

Valuation, May 29, 2015

P/E [x] 7.20 15.80 21.30 14.80

P/BV [x] 1.20 2.90 3.40 2.50

Source: Bloomberg, PEFINDO Research & Consulting - Equity & Index Valuation Division Estimates

Table 5: Summary of GCM Method Valuation

Multiples

(x)

Est. EPS

(IDR)

Est. BV/Share

(IDR)

Value

(IDR)

P/BV 2.50 - 539 1,363

P/E 14.80 109 - 1,603 Source: Bloomberg, PEFINDO Research & Consulting - Equity & Index Valuation Division Estimates

Table 6: Fair Value Reconciliation Fair Value per Share [IDR]

DCF GCM Average

Upper limit 1,096 1,603 1,250

Bottom limit 940 1,363 1,065

Weight 70% 30%

Source: PEFINDO Research & Consulting - Equity & Index Valuation Division Estimates

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 10 of 11

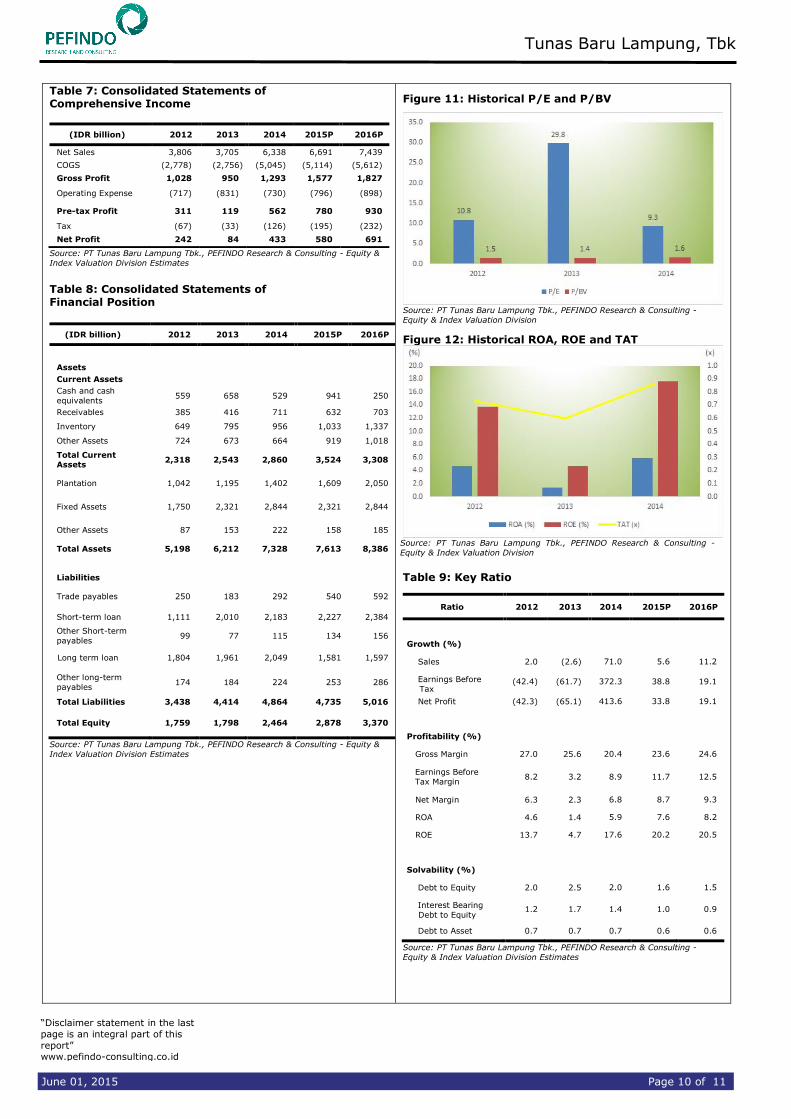

Table 7: Consolidated Statements of Comprehensive Income

(IDR billion) 2012 2013 2014 2015P 2016P

Net Sales 3,806 3,705 6,338 6,691 7,439

COGS (2,778) (2,756) (5,045) (5,114) (5,612)

Gross Profit 1,028 950 1,293 1,577 1,827

Operating Expense (717) (831) (730) (796) (898)

Pre-tax Profit 311 119 562 780 930

Tax (67) (33) (126) (195) (232)

Net Profit 242 84 433 580 691

Source: PT Tunas Baru Lampung Tbk., PEFINDO Research & Consulting - Equity &

Index Valuation Division Estimates

Table 8: Consolidated Statements of Financial Position

(IDR billion) 2012 2013 2014 2015P 2016P

Assets

Current Assets

Cash and cash

equivalents 559 658 529 941 250

Receivables 385 416 711 632 703

Inventory 649 795 956 1,033 1,337

Other Assets 724 673 664 919 1,018

Total Current Assets

2,318 2,543 2,860 3,524 3,308

Plantation 1,042 1,195 1,402 1,609 2,050

Fixed Assets 1,750 2,321 2,844 2,321 2,844

Other Assets 87 153 222 158 185

Total Assets 5,198 6,212 7,328 7,613 8,386

Liabilities

Trade payables 250 183 292 540 592

Short-term loan 1,111 2,010 2,183 2,227 2,384

Other Short-term

payables 99 77 115 134 156

Long term loan 1,804 1,961 2,049 1,581 1,597

Other long-term

payables 174 184 224 253 286

Total Liabilities 3,438 4,414 4,864 4,735 5,016

Total Equity 1,759 1,798 2,464 2,878 3,370

Source: PT Tunas Baru Lampung Tbk., PEFINDO Research & Consulting - Equity &

Index Valuation Division Estimates

Figure 11: Historical P/E and P/BV

Source: PT Tunas Baru Lampung Tbk., PEFINDO Research & Consulting -

Equity & Index Valuation Division

Figure 12: Historical ROA, ROE and TAT

Source: PT Tunas Baru Lampung Tbk., PEFINDO Research & Consulting -

Equity & Index Valuation Division

Table 9: Key Ratio

Ratio 2012 2013 2014 2015P 2016P

Growth (%)

Sales 2.0 (2.6) 71.0 5.6 11.2

Earnings Before

Tax (42.4) (61.7) 372.3 38.8 19.1

Net Profit (42.3) (65.1) 413.6 33.8 19.1

Profitability (%)

Gross Margin 27.0 25.6 20.4 23.6 24.6

Earnings Before

Tax Margin 8.2 3.2 8.9 11.7 12.5

Net Margin 6.3 2.3 6.8 8.7 9.3

ROA 4.6 1.4 5.9 7.6 8.2

ROE 13.7 4.7 17.6 20.2 20.5

Solvability (%)

Debt to Equity 2.0 2.5 2.0 1.6 1.5

Interest Bearing

Debt to Equity 1.2 1.7 1.4 1.0 0.9

Debt to Asset 0.7 0.7 0.7 0.6 0.6

Source: PT Tunas Baru Lampung Tbk., PEFINDO Research & Consulting -

Equity & Index Valuation Division Estimates

“Disclaimer statement in the last

page is an integral part of this

report” www.pefindo-consulting.co.id

Tunas Baru Lampung, Tbk

June 01, 2015 Page 11 of 11

DISCLAIMER

This report was prepared based on trusted and reliable sources. Nevertheless, we do not

guarantee its completeness, accuracy and adequacy. Therefore, we are not responsible for any investment decisions made based on this report. All assumptions, opinions and predictions were

solely our internal judgments as of the reporting date, and those judgments are subject to

change without further notice.

We are not responsible for any mistakes or negligence that occurs by using this report. Recent

performance cannot always be used as a reference for future outcome. This report does not offer a recommendation to purchase or hold particular shares. This report might not be suitable

for some investors. All opinions in this report have been presented fairly as of the issuing date

with good intentions; however, they could change at any time without further notice. The price, value or income of each share of the Company stated in this report might be lower than

investor expectations, and investors may obtain returns lower than the invested amount.

Investment is defined as the probable income that will be received in the future; nonetheless such returns may fluctuate. As for companies whose shares are denominated in a currency

other than Rupiah, foreign exchange fluctuation may reduce their share value, price or the

returns for investors. This report does not contain any information for tax considerations in

investment decision-making.

The share price target in this report is a fundamental value, not a fair market value or a transaction price reference required by regulations.

The share price target report issued by the PT PEFINDO Riset Konsultasi (“PRK”) or “PEFINDO Research and Consulting” is not a recommendation to buy, sell or hold particular shares. It

should not be considered as investment advice from the PRK and its scope of service to some

parties, including listed companies, financial advisors, brokers, investment banks, financial institutions and intermediaries, does not correlate with receiving rewards or any other benefits

from such parties.

This report is not intended for any particular investor and cannot be used as part of an

objective investment analysis of particular shares, an investment recommendation, or an

investment strategy. We strongly recommend investors to consider the suitability of the situation and conditions before making a decision in relation with the figures in this report. If

necessary, consult with your financial advisor.

PEFINDO keeps the activities of the Equity Valuation Division separate from its Ratings Division

to preserve the independence and objectivity of its analytical processes and products. PEFINDO

has established policies and procedures to maintain the confidentiality of non-public information received in connection with each analytical process. The entire process, methodology and the

database used in the preparation of the Reference Share Price Target Report as a whole are

different from the processes, methodologies and databases used by PEFINDO in issuing ratings.

This report was prepared and composed by PRK with the objective of enhancing the

transparency of share prices of listed companies in the Indonesia Stock Exchange (IDX). This report is also free of influence from any other party, including pressure or force either from IDX

or the listed company reviewed. PRK earns reward from IDX and the reviewed company for

issuing this report twice a year. For further information, please visit our website at http://www.pefindo-consulting.co.id

This report was prepared and composed by the PEFINDO Research & Consulting - Equity &

Index Valuation Division. In Indonesia, this report is published in our website and in the IDX website.

Related Documents